6 Things To Consider Before Taking Out A Mortgage

Some posts contain affiliate links, see disclosure for more details.

Are you considering taking out a mortgage and getting on the property ladder? There’s no denying that it’s a strange time to be moving house at the moment, but despite the current situation throughout the world people are still needing and wanting to move house for lots of various reasons, like growing families, changes in employment and so on.

The good news is that it’s still possible to buy and sell houses at the moment, although some things will of course be different, for example you may have to have virtual viewings or valuations.

We started thinking about moving house just before lockdown happened in early 2020. Ideally we want to be closer to good secondary schools, and not so far out of town. We managed to view a few houses while restrictions were in place and over the summer but quickly found that estate agents were getting stricter about allowing us to view properties without already having a mortgage agreement in place.

Before we could get any further, one isolation period seemed to follow another, with the kid’s school closing and us having to stay home and next thing we’ve in full lockdown again with all plans put on hold for now (although I do still love to look online at houses for sale!)

Fingers crossed though we can get things going again by Spring. Despite the struggles caused by the pandemic, according to experts homeownership levels are predicted to rise.

Since this is our second time of needing to take out a mortgage and we’ve picked up a few things from last time, here are some tips on the things you should consider before taking on a mortgage.

1. Saving a deposit

To be able to take out a mortgage you’ll need to have saved up some kind of a deposit to put down. Usually this will need to be at least 5% of the value of the house, and ideally more.

How much deposit you have will affect how much mortgage you need to take out, the length of mortgage you’ll need and the overall amount of interest you’ll pay over the course of the mortgage.

2. Your budget/what you can afford

The main thing of course will be to work out what you can afford. How much money can you afford to pay off the mortgage each month, bearing in mind all your other money outgoings. Is your income stable? The bank will want to look at your income, and the stability of it before approving you for lending.

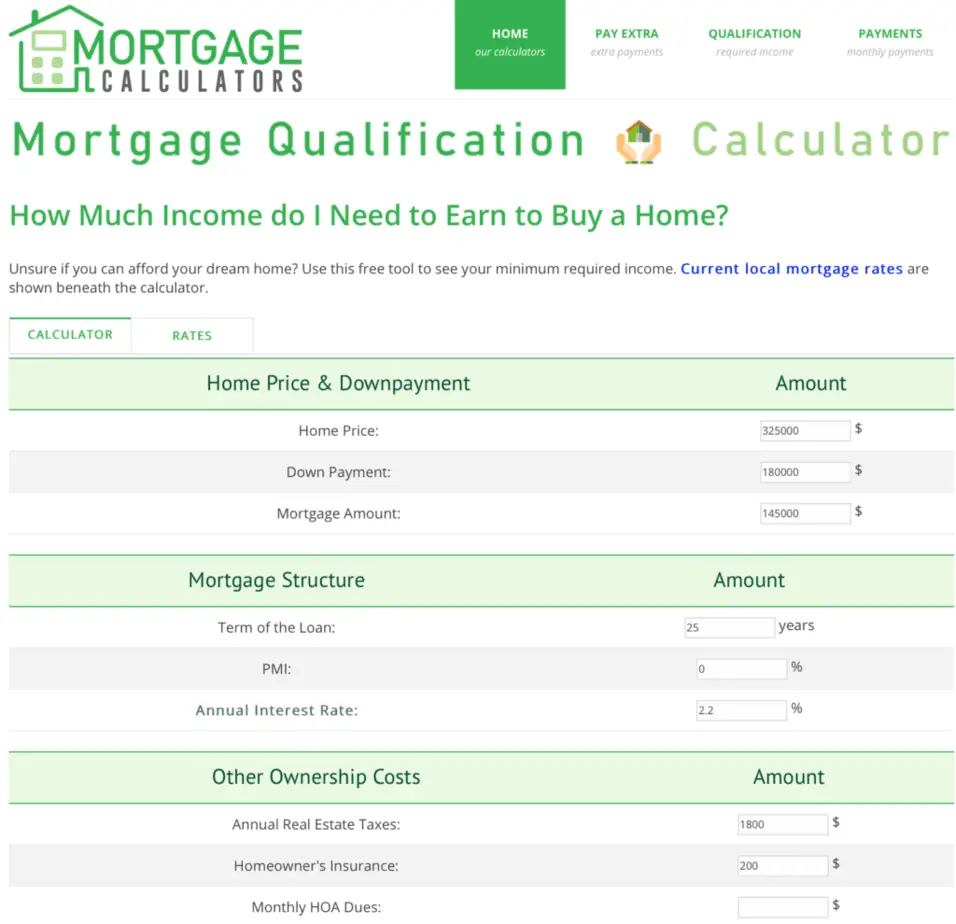

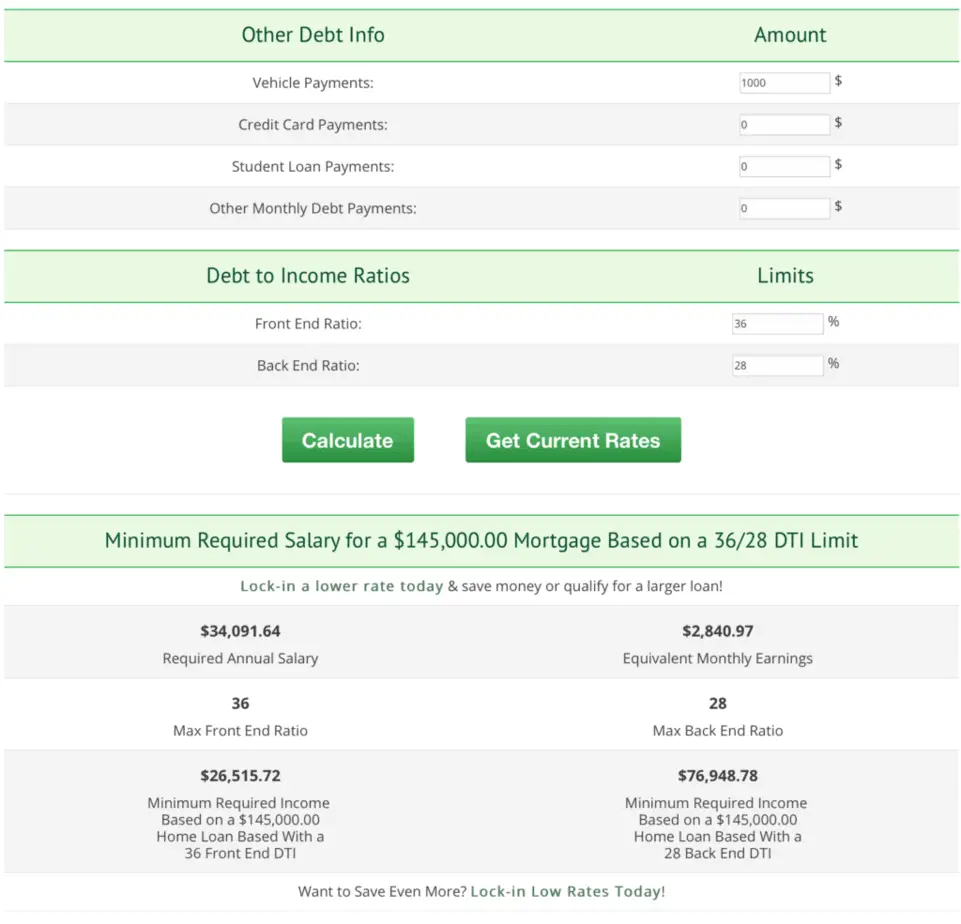

You can even use a calculator like this one from MortgageCalculators.info to pop in all your details and see whether your income and outgoings mean you can afford what you’re looking for.

It’s worth comparing how different lengths of mortgages and interest rates will affect monthly payments, and seeing how adjusting the amount you pay each month can make a difference to how long a term of mortgage you’ll need, along with how much interest you’ll pay back.

3. Existing debt

Don’t forget to factor in any existing debt you already have, as the banks will definitely consider these before approving a mortgage. It’s a good idea to try and clear these first, as you’ll want to be able to show you are capable of paying back borrowed money.

4. Your credit score

Your credit score will have an impact too – this will be looked at when you make a mortgage application, so the higher your score, the better. This shows your debt to income ratio, current borrowing and repayment history.

You can improve your score by:- Making sure you’re on the electoral roll

- Always paying bills on time

- Checking your financial links

- Minimising credit applications

- Checking your credit file

- Not withdrawing cash from credit cards

5. Extra fees

Don’t forget when you’re buying a house there are other costs to consider. You may want to pay for a survey, to make sure the house is structurally sound, solicitors fees and stamp duty.

6. Using a broker

To find the best mortgage for you it might be easiest to use a mortgage broker. A broker will be able to take your specific circumstances and search out the best mortgage deals available to you.

You may also like: