Quick Guide To Personal Loans – #Ad

Some posts contain affiliate links, see disclosure for more details.

If you’re wanting to cover the costs of a large expense (like needing a new car) but don’t have enough money to pay upfront, you might have thought about taking out a personal loan.

When it comes to borrowing money, it’s always best to be as informed as you can be. Make sure you’re aware of how borrowing money can affect your finances and that you’re able to afford the monthly repayments without falling behind and deepening the debt.

HSBC have created this Quick Guide to Personal Loans to highlight the key information you need to know when it comes to personal loans.

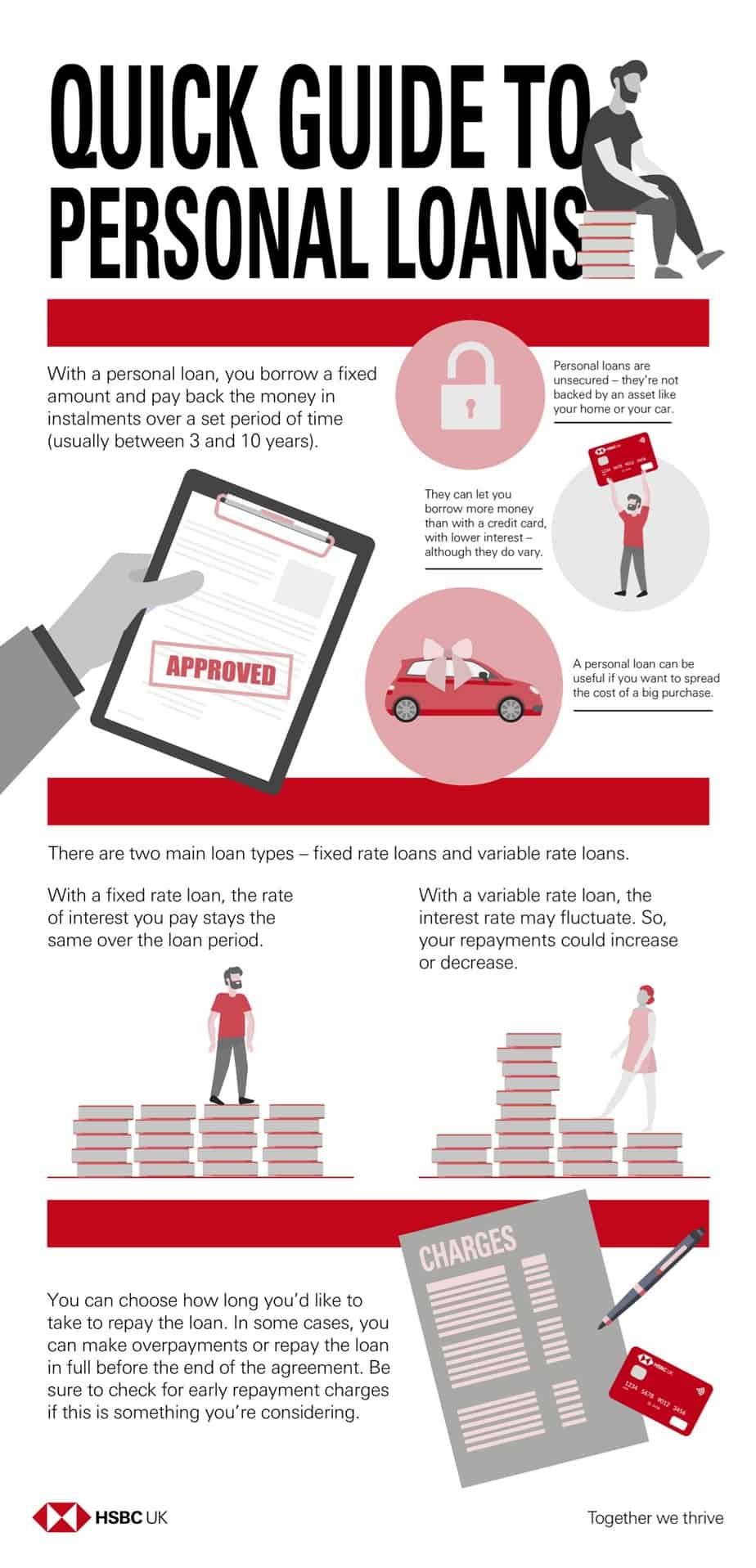

What is a personal loan?

A personal loan is when you borrow a fixed amount of money and pay it back in a series of installments over a predetermined period of time.

A personal loan is what’s known as an unsecured loan. This means it’s not tied to any of your assets, like your home or car.

You would usually use a personal loan when wanting to borrow a larger amount of money over a longer period of time than you might use a credit card for, and the interest rates are usually, though not always, lower than with a credit card.

There are two main loan types, a fixed rate loan and a variable rate loan. With a fixed rate loan, the rate of interest you pay remains the same throughout the loan period.

With a variable rate loan, the interest rate may vary, meaning your repayments could go up or down.

When might you want a personal loan?

You might consider taking out a personal loan when you’re looking to cover a larger expense, such as making home improvements, buying a new car or perhaps the cost of getting married.

You could also use a personal loan, such as HSBC personal loans, to consolidate debts to make them more manageable.

Things to consider before applying for a personal loan.

- How much you need to borrow – work out how much you’ll need to borrow for your project, make sure to budget for all the predicted costs involved.

- How much you can afford to repay – work out how much you’ll be able to pay back each month.

- How long you want to borrow for – borrowing for a longer period of time may mean your monthly repayments are lower, but it also means you will likely pay more interest overall over the course of the loan.

- The APR – this is the annual percentage rate on the loan which will vary between different loans, and may also vary depending on your credit rating and current financial situation.

- Other factors – you might want to consider things such as whether there are any fees if you wish to pay back the loan early or make overpayments, or how quickly you will receive the loan money.

You might also like:

7 Simple Steps to Pay Off Debt Faster >>