Saving For Retirement: Tips For Planning Ahead

Some posts contain affiliate links, see disclosure for more details.

When you’re young and fairly early on in your career, saving for retirement may not even be on your radar. It still feels a long way off, a future event you don’t need to think about yet.

But actually, when it comes to planning for retirement, time is your friend. Starting to save for retirement early can be the best financial gift you can make to your future self.

Twenty-two percent of Americans have less than $5,000 saved for retirement, and 15 percent have no retirement savings whatsoever.

Annuity.org

With many Americans having no retirement savings, and the average women’s savings being less than half that of men, it’s not surprising that according to Forbes, more than 75% of Americans fall short when it comes to conservative savings targets for retirement.

When to start saving for retirement

If you want to ensure you have enough savings for retirement, you need to have a good retirement strategy. The best time to start saving is now. It’s never too late, but the earlier you start saving, the lower your savings need to be as they’ll have longer to grow.

Compound interest means smaller amounts saved early can grow bigger than larger amounts invested later on.

How much should you save?

How much you need to have saved for retirement will depend of course on a variety of factors, such as health, family, current income, how much you think you’ll need or want to live on and so on.

The amount of money you are able to save will depend on your income and outgoings, but as a general rule of thumb, Fidelity recommends a savings amount of 15% of your pre tax income is enough to maintain a steady retirement income that will last into your early 90s.

How to work out what’s right for you

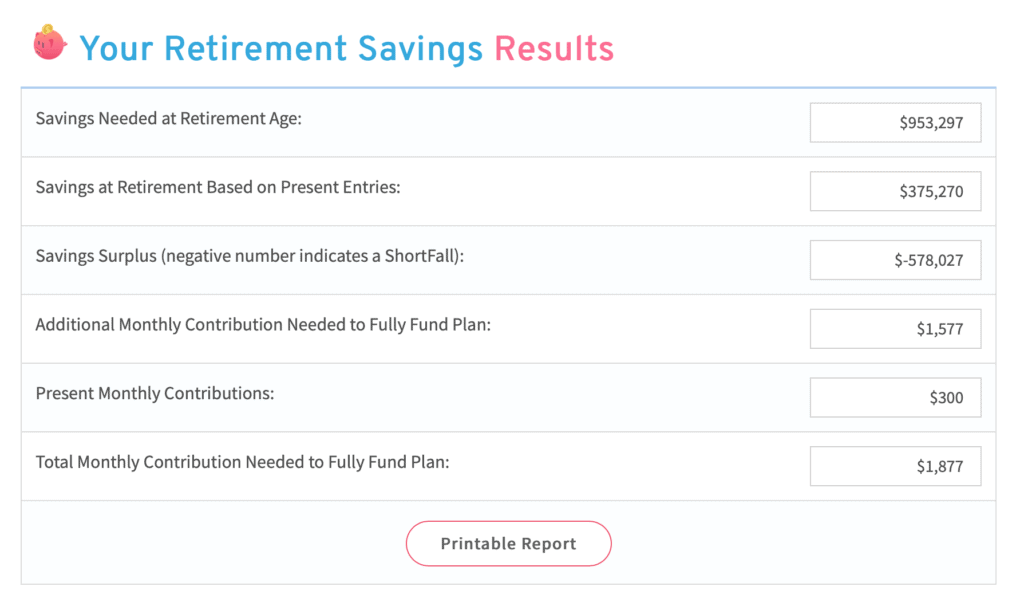

If you want to have a good estimate of how different amounts of savings can affect your retirement income, using a retirement calculator such as this one from Pigly, means you can work out how much you’ll need to save based on the age you want to retire at.

You can adjust the amounts to see how varying the age, length and amount of income you expect to need for your retirement will affect the amount you need to save, as well as accounting for any retirement funding you’re currently receiving and any savings you have already accrued.

You can even print out the report to help with your financial planning.

Quick Tips for Retirement Savings

- Make retirement savings a priority – while you may not be able to make the same amount of savings every month (we all have things like unexpected expenses, lower income months, childcare bills that affect our finances) regular saving is key to building a good retirement income.

- Balance your current and future financial needs – Whether you have debt to pay now, your current income levels, whether you’re considering a lump sum pension and what age you plan on claiming social security retirement benefits will all impact your financial planning – the CFPB have lots of tools and information to help you plan.

- Create a budget – If you don’t already have one, drawing up a budget is critical to helping with managing money, not just for retirement planning but for keeping your everyday finances healthy and under control.

- Don’t touch your savings – If it’s at all avoidable, don’t touch your retirement savings! If you withdraw early you may pay penalties and lose principal and interest. Try and keep your savings in your retirement plan or an IRA.

Finally, don’t panic. If you haven’t already started saving for retirement, it’s never too late or too early! If you start saving and stick to it you’re much more likely to reach your retirement goals.