8 Psychological Savings Tips – Trick Your Brain to Save Money

Some posts contain affiliate links, see disclosure for more details.

If you’re here, you’re probably looking for some tips to save money. You’re in luck, because two things that I love are saving money and learning how the brain works. In this post, you’ll learn how to save money using some psychological tricks to make your goals easier to achieve.

There are many reasons to save money. You could be saving up for a big trip, it could be a fun gadget you want, or it could be just to prepare for unfortunate times. No matter what the reason is, it’s always a good idea to have some cash saved.

1. Pay in Cash

Yeah, this is a simple one, but it works. I can’t count how many times I’ve used my credit card in the past month, but I bet it’s over 100. Paying in cold, hard physical cash will cause 2 things to happen. One, you will physically hurt handing over money. It’s been proven in a few studies.

Two, it’s psychologically easier to spend smaller bills than it is to spend larger bills because our brains see them as a “scarce” and valuable resource. We are hardwired to want to hoard these resources for future use.

In fact, watching someone burn a $20 bill will light up the brain more than watching someone burn a $1 bill. You can guess what it does when they watch someone burn a $100.

Paying in cash also gives you a clear idea of how much you have left. Unlike a credit card, the currency is physical and limited, instead of “imaginary” and seemingly unlimited.

2. Keep a Change Jar

Secondly, if you pay in cash, you will likely accumulate quite a bit of change. Quarters, dimes, nickels, they all add up. I suggest keeping these in your pockets throughout the day and depositing them into a covered jar at night. Why keep it covered? One day you’ll stick a quarter in and you’ll realize it wont fit. This means you’ve filled it up.

For me personally, one year I turned it into a game to guess how close I was to filling up my jar. Even a dollar a day is enough to pay off Netflix, Hulu, and a few cups of coffee. If you’re looking for ways to cut costs, you may find this article on funny ways to save money helpful.

3. Use a 2% cash back card

I don’t recommend using a credit card to pay if you’re trying to save money, but if you are, be smart about it. There are a few cards that will give you 2% back on EVERY purchase, but due to the changing nature of credit cards, I won’t list them here. Some even offer up to 5% if you pay close attention to their seasonal rewards.

Personally, I own a small business and buy things with a 2% cashback card. I never really see that cashback until specifically log in to cash out (since I use automatic payments, something we’ll talk about next).

The magic is in the fact that I don’t use my credit card to buy anything I wouldn’t buy anyways. For example, I have to pay my website host, a few third party software services, advertising costs, and writers. I could have paid with my debit card, but since I use a 2% back, I essentially earned a tax-free amount of over $1000 FREE last year.

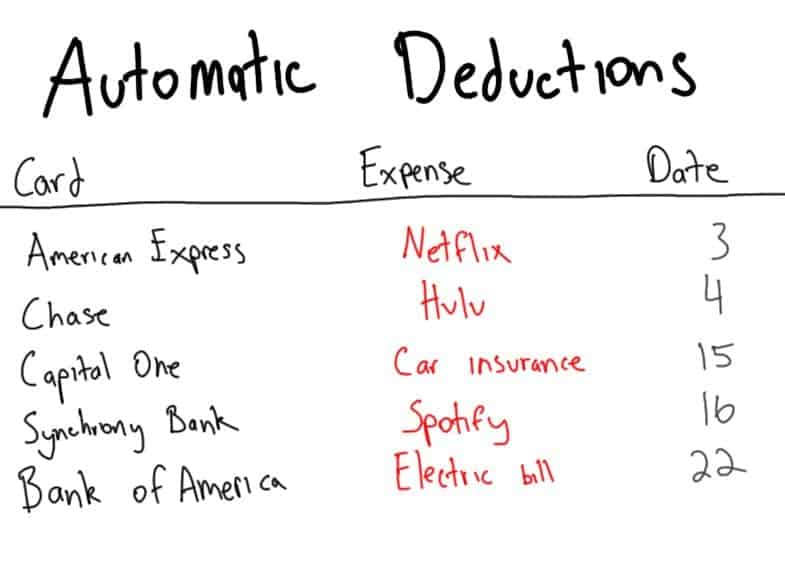

4. Automatic deductions

If you can, set up automatic deductions to make your monthly budget easier. I do my budget every 3-4 days to check my numbers, and setting up automatic deductions makes it easier. Psychologically, since it is easier, I will not only be more likely to pay the bill, but it will also be easier to keep track of where the money is going.

Here’s an image of my monthly personal budget, along with the dates of each:

5. Round up savings

Some banks offer a service called “Round Up Savings” that will round up any purchases on your debit card to the nearest dollar. The difference is then deposited into a seperate savings account. For example, if you bought a coffee for $2.25, $.75 will be automatically deposited into your savings account.

My girlfriend absolutely loves this, and has saved $75 so far this year with it. It’s very neat if you don’t want to get tangled up with keeping track of credit cards.

6. Ask what an item truly is worth

A lot of times, we buy things not because we need them, but because we want them based on fantasizing. For example, I once bought a car that was more expensive than it needed to be, but I knew that I would look “super cool” in it.

Three years later, it stopped being cool but the bank kept wanting payments. Needless to say, I learned how much people really don’t care about what car you drive.

We often fall prey to something called the anchoring bias: the effect that occurs when the value of something is based on your initial reaction to it. For a quick example, if I had a TV that was valued at $1000, and I bought it for $800… I’d feel great.

However, if I saw the exact same TV a week ago listed for $600, but now they raised the price to $800, I would not feel so great about paying the $800. Instead, you should determine the true value of the item you’re buying.

My car’s extrinsic value was to get me back and forth to work reliably. Really, the only difference between a $10,000 car and a $25,000 car is usually comfort (and not a $15k difference, mind you).

Ask what practical use an item has to you, and then compare this to the price you plan on paying for it. Taking time to weigh the pros and cons of a purchase can help you save money.

Here’s another psychological trick to help put things in perspective:

7 . Turn prices into hours

Many people get paid for every hour they put in. For example, if you get paid $16/hour, and work 8 hours, you will earn $128. We both know this is not what you keep, because taxes have to be taken out. Let’s assume a 20% tax rate, this means you get to keep $102.40 of that.

So the next time you book a hotel room on vacation, or upgrade to a new phone, go ahead and calculate how many hours you would have to work to actually afford it.

To buy a Macbook Pro 16” in March 2020, you would have to work just over 187 hours at $16/hour with a 20% tax rate. That’s a whole 23 days to afford a Macbook.

To afford a $20,000 car on the same budget, you’d have to work a total of 39 weeks (1562 hours). This isn’t even mentioning insurance, gas, and maintenance!

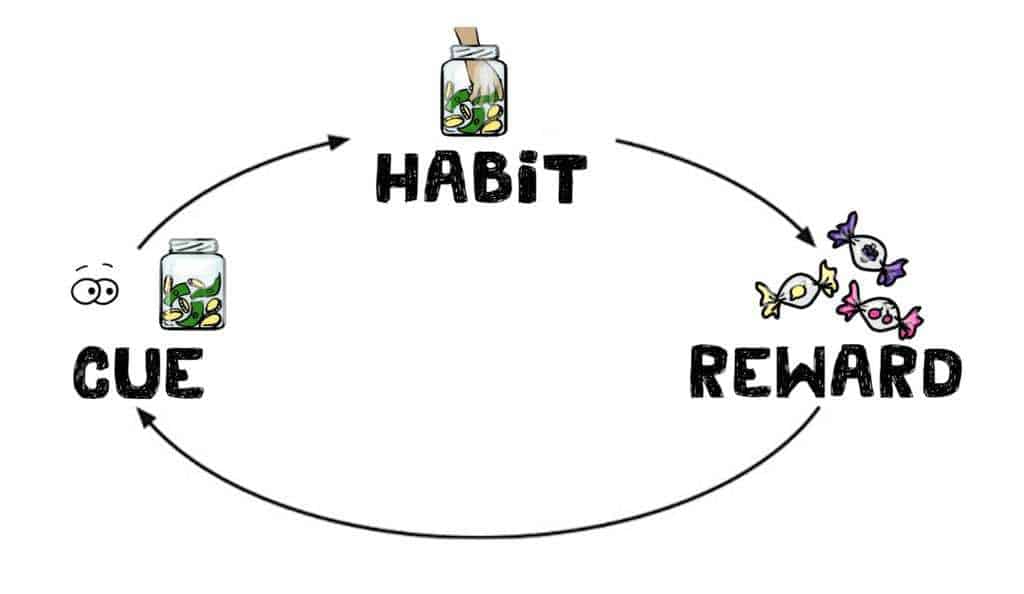

8. Make it a habit to save money

Psychologists have found that habits are formed when a 3-step process is followed.

First is the cue. This is anything that reminds you of the habit. For example, right when I step out of the shower, I’m in front of the mirror ready to brush my teeth. I don’t think I could skip it if I wanted to!

Second is the actual habit. The trick with implementing the habit is to keep it as simple as possible. If I wanted to make running in the morning a habit, I would set my running clothes by my bed, my shoes by the door, and plug in my headphones before I went to sleep.

This way I could wake up, change, put on my shoes and make the process of running as easy as possible. If you want to save money, do the same thing – make it simple.

Third is the reward. Along with our running analogy, I would drink some coffee right after my run. Why? Because I am a coffee lover and it would be satisfying to me – it would be a great reward. Habits stick because of their rewards. People smoke because of the nicotine “high”.

Give yourself a small reward when you actually save money. Whether it be as simple as a piece of candy or as elaborate as asking your friend to cheer you on, a reward will ensure it continues.

These are eight psychological tricks I’ve used to help me and my girlfriend save money, and I hope you’ve found them useful.

Author Bio

Theodore Thudium is the author, marketer, and Youtuber who founded Practical Psychology. His goal is to help people improve their lives by understanding how their brains work. He specializes in condensing research material into entertaining, digestible, and useful content for the everyday psychology enthusiast.

Read More:

Pin it!