Quick Tips For Creating A Family Budget

Some posts contain affiliate links, see disclosure for more details.

Food, bills, school uniform, clubs, more bills, classes, clothes, presents, childcare – the costs of general family life can quickly add up! Without a family budget, it can be easy to let these costs run away from us.

Even now, in these strange circumstances where we might not have all those extra expenses – for example childcare not currently being used, clubs and classes cancelled – a lot of us are facing tougher financial circumstances due to being out of work or unable to earn, or having to juggle working from home and ‘home-schooling’ our children.

Personally, we are finding the cost of a normal grocery shop is much more expensive than usual, whether that’s because promotions are less, prices are higher, or just because the kids seem to want to eat 7832 times a day!

Whatever your situation, creating and using a household budget is a good way to keep on top of family finances.

Here are some quick tips to set up a family budget.

Start With A Financial Check Up

Getting a good overview of where your finances are at is a good place to start! Gather together all your documents (open them up online if you don’t use paper copies) – include payslips, bills, bank statements and so on. Everything that shows money coming in, or going out.

Next you want to go through everything to get a picture of where your money is going. Make a note of all your outgoings, where is your money being spent? Try not to leave anything out.

To get a really good overview of where your money is going, you could try using a spending tracker for a couple of weeks.

Here’s an example of things you might include on your list:

- Rent/mortgage

- Electricity

- Gas

- Water

- Broadband

- Mobile Phone

- TV Licence

- Groceries

- Council tax

- Car running costs

- Insurance (car/home/life)

- Debt repayments

- Netflix/Amazon/Sky

- Kids clubs (dance/swimming/scouts etc)

- Eating out/Takeaways

- Memberships -eg. gym

- New clothes

- Gifts

- Holidays

Next do the same for your income. What sources of income do you have? Include any wages from members of your household, child benefit, other benefits and any extra income streams.

Split Spending Into Essential and Non Essential

The next thing to do is to separate your outgoings into essential and non-essential spending.

Essential spending will include things like mortgage payments or rent, utility bills and groceries, kids school supplies etc. All the basics you need to live.

Non essentials might include things like television subscriptions, gym memberships, money spent on takeaways or social outings.

Add up all your essential outgoings and compare against your total income. If your income exceeds your outgoings, that’s great! Whatever amount is left can either be used towards your non essential spending, disposable income or put towards savings.

If your income doesn’t cover your essential spending, you might want to look at seeing if there’s anyway to lower your bills and expenses – you might be able to switch to a cheaper energy provider or change tariff. You can also check if you’re entitled to any help.

Another idea could be to look at ways to earn extra money on the side.

Set Financial Goals

While you’re making your budget, it’s a good time to think about any financial goals you might have. This could be anything but some examples might be to save a deposit for a family home, pay off debt, or plan for a holiday.

To help figure out how long it might take to reach your goals, you could try using Calculator.me’s savings calculator, which will show how your savings will grow over time.

You can then incorporate those goals into your budget which can help you work out how to achieve them.

Decide On A Budgeting Strategy

There are a few different budgeting strategies, and people find that one style tends to suit them better than others. Popular methods include:

Zero based budgeting – this is my favourite, as it accounts for every penny. With a zero based budget you allocate all the income, right down to zero. The goal is to have nothing left, because you’ve given everything a purpose – whether that’s bills, debts, savings or anything.

This is a great budgeting method if you want to be more intentional with spending, avoid any waste and like having a detailed account of your finances.

Read more: How To Use A Zero-Based Budgeting System To Manage Money >>

50/30/20 budgeting – also known as percentage budgeting.

With this strategy, you divide your money between needs, wants and savings (and/or debt repayments).

After tax, you would set aside 50% of your income for needs – this accounts for all your essentials, i.e mortgage, rent, utilities, food. 30% is then allocated towards ‘wants’. These are things that are non essential spending, for example, eating out, leisure activities and so on.

The remaining 20% goes towards savings or debt repayments.

The downside of this type of budget is that those percentages might not work for everybody. The upside is you can be flexible, but it’s best to try and reduce the ‘wants’ category first, rather than the savings category.

Read More: 9 Easy Budgeting Strategies To Improve Finances >>

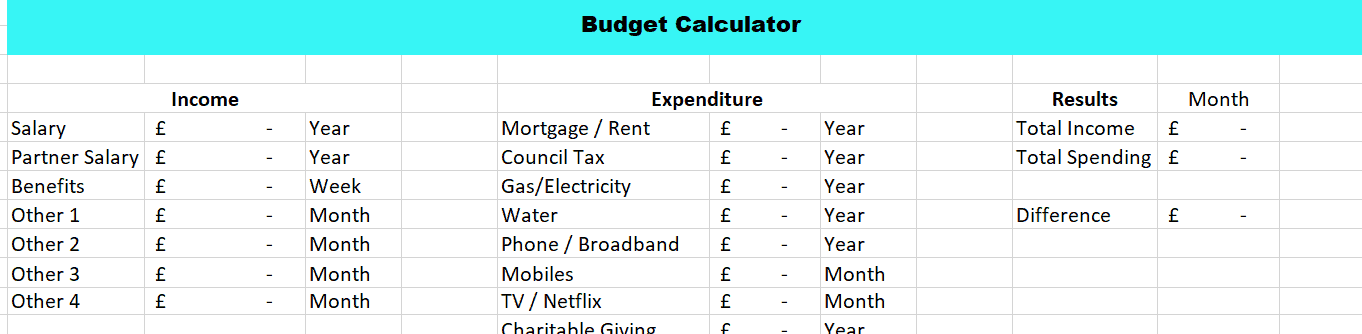

Some people prefer to budget on pen and paper, others like to use a spreadsheet (here’s the basic spreadsheet we use – you can download and adapt to create your own).

There are also lots of great budgeting apps available that you can link up to your bank for help budgeting – I like YNAB for this, and Monzo is a banking app that can help with budgeting especially if you like to see your money in separate ‘pots’.

Getting Out Of Debt

Whichever type of budget you decide to go for, if you’re currently in debt, you’ll want to make sure to include debt repayments as part of your budgeting strategy.

National Debtline have a great online tool that can help you work out a budget, it’s particularly helpful for working out a budget when you have a lot of debt, but also a really handy tool even if you’re already debt free, including lots of categories you might not necessarily have remembered to include in your budget.

Read more: 9 Simple Ways To Pay Off Debt Faster >>

Building An Emergency Fund

Another helpful thing to try and include as part of your monthly family budget is saving an emergency fund. Having money set aside to cover any unexpected emergencies can be a lifesaver and stop you having to rely on credit or get further into debt.

Read more: How To Build An Emergency Fund (Even When You Think You Can’t Afford To) >>

When you’re building a family budget it’s really useful to get everyone on board with it. If everyone’s working towards the same goals and spending with similar intentions a family budget can work really well.

Whilst children might be too young to need to know the full financial ‘ins and outs’, studies have shown that good money habits start to develop at a really young age, so it’s a great time to get them involved with money saving efforts.

Read more: How To Teach Kids About Money >>

While you’re planning ahead, it’s a good time to think about whether it’s a good idea to invest in life insurance, and set up a will. It can seem a bit morbid to think about financial implications should anything happen, but it’s simple to do and once you’ve ticked it off the to-do list it can give you peace of mind.

Keeping On Top Of Your Budget

Having monthly budget meetings is a great way to keep on top of your budget. It means you can see how well it’s working and whether you need to make adjustments anywhere to keep on track – you can be flexible and move things around where necessary.

Lastly:

Don’t forget to budget for the fun stuff too. Lots of people put off making a budget, thinking it’s all doom and gloom and too strict and boring. Including the fun things in your budget means you can enjoy yourself without worrying about overspending, knowing you’ve got the dedicated funds there.

Related Reading:

Budgeting resources

Here are some budgeting resources for help creating and maintaining a budget:

- Budget spreadsheet/calculator – our handy spreadsheet you can adjust to make your own, it does all the maths for you.

- Budgeting With Debt Tool from National Debtline

For those that prefer putting pen to paper:

- Free printable Monthly Budget Planner from MoneySavingCentral.com

- Spending Diary – free printable from Skintdad.co.uk

- Free budgeting worksheets from BudgetingIsAChallenge.com

- Free Debt Trackers & more from TheMoneyFox.com

Pin it!